What Is An All In One Loan

Let's face it: most of us love the feeling of control, especially when it comes to our finances. We relish the idea of optimization, of making our money work harder for us. That's where the allure of an all-in-one loan comes in. It promises a streamlined, potentially more efficient way to manage a significant chunk of your debt. But is it right for you?

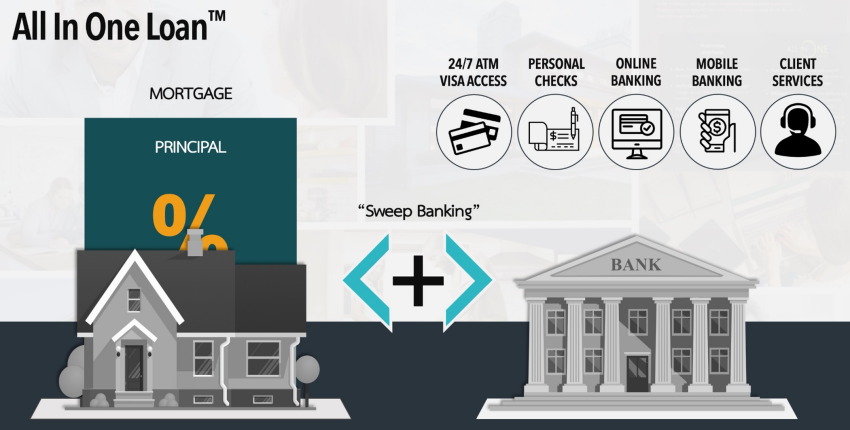

An all-in-one loan, also known as a mortgage payoff accelerator, is essentially a hybrid between a mortgage and a checking account. Think of it as a line of credit secured by your home equity. Instead of your paycheck going into a regular checking account and then being used to make your mortgage payment, it goes directly into this all-in-one loan account. This immediately reduces the principal balance on which interest is calculated. As you spend money, your balance increases, and so does the interest you owe, but any idle money actively chips away at your mortgage.

The primary benefit is the potential to significantly shorten the life of your mortgage and save a substantial amount on interest. Because your balance is constantly fluctuating based on your deposits and withdrawals, you’re theoretically paying down the principal faster. It's like constantly making extra payments without the pressure of committing to a fixed amount. Another perceived benefit is the flexibility. Need to tap into some equity for a home renovation or unexpected expense? The funds are readily available within your credit limit.

Must Read

Common examples of applying this involve homeowners who are very disciplined with their budgeting. Imagine a freelancer who deposits irregular income into their all-in-one loan. Each large deposit drastically reduces the principal, offsetting the impact of subsequent withdrawals for expenses. Similarly, someone receiving a large bonus or inheritance could use it to make a substantial dent in their mortgage principal, accelerating their payoff timeline.

However, simply having an all-in-one loan isn't a magic bullet. To truly maximize its benefits, strategic planning is crucial. Here are some practical tips to enjoy it more effectively:

- Meticulously Track Your Spending: Knowing where your money is going is paramount. A detailed budget will help you identify areas where you can cut back and allocate more funds towards reducing your loan balance.

- Aggressively Pay Down the Principal: Aim to deposit any extra cash – bonuses, tax refunds, even small windfalls – directly into the loan to maximize the interest savings.

- Avoid Overspending: The ease of access to credit can be a double-edged sword. Resist the temptation to use the line of credit for unnecessary purchases, as this will negate the benefits of accelerated payoff.

- Compare Interest Rates: All-in-one loans often come with variable interest rates. Understand how these rates fluctuate and compare them to traditional mortgage rates to ensure you're getting a competitive deal.

- Understand the Fees: Be aware of any fees associated with the loan, such as origination fees, annual fees, or transaction fees, and factor them into your calculations.

Ultimately, an all-in-one loan is a powerful tool, but it requires a proactive and disciplined approach to financial management. When used correctly, it can be a game-changer in your journey towards becoming mortgage-free faster. But if you're not prepared to actively manage your finances, a traditional mortgage might be a more suitable option.